Fillable Montana Promissory Note Template

Fillable Montana Promissory Note Template

In the vast and beautiful state of Montana, financial transactions often require clear agreements to ensure that both parties understand their obligations. One such agreement is the Montana Promissory Note form, a vital tool for individuals and businesses alike. This form serves as a written promise to pay a specified amount of money to a lender at a designated time or on demand. It includes essential details such as the principal amount, interest rate, repayment schedule, and any late fees that may apply. By outlining these terms, the Promissory Note helps prevent misunderstandings and provides legal protection for both the borrower and the lender. Whether you’re securing a loan for a new home, financing a vehicle, or simply borrowing money from a friend, understanding how to properly utilize this form can make all the difference in ensuring a smooth transaction. With a clear structure and straightforward language, the Montana Promissory Note form empowers individuals to engage in financial agreements with confidence.

Incorrect Borrower Information: Failing to provide the full legal name and address of the borrower can lead to confusion. Ensure that the borrower’s information is accurate and up-to-date.

Missing Lender Details: Just like the borrower, the lender’s name and address must be clearly stated. Omitting this information can complicate the enforcement of the note.

Ambiguous Loan Amount: Specifying the loan amount is crucial. If the amount is unclear or written incorrectly, it may lead to disputes later on.

Interest Rate Errors: If an interest rate is applicable, it must be clearly defined. Mistakes in this section can lead to misunderstandings about repayment obligations.

Failure to Specify Payment Terms: It is important to outline how and when payments will be made. Without clear terms, borrowers may not understand their obligations.

Neglecting Signatures: Both the borrower and lender must sign the document. A missing signature can render the note unenforceable.

Not Keeping Copies: After filling out the Promissory Note, both parties should retain copies. This helps in maintaining a record of the agreement and can be essential if disputes arise.

Letter of Quit Notice From Landlord to Tenant - If the tenant vacates the property before the specified date, they may avoid further legal action.

Utilizing a Free And Invoice PDF form can significantly streamline your business processes, allowing for seamless record-keeping and enhancing the professionalism of your transactions. For those looking to create such forms efficiently, tools available at smarttemplates.net can be incredibly helpful in generating customizable templates that meet various business needs.

Selling a Vehicle in Montana - The ATV Bill of Sale fosters trust between the buyer and the seller.

State of Montana Employee Handbook - Understand how to effectively utilize employee resources for personal and professional growth.

When filling out the Montana Promissory Note form, it is important to follow certain guidelines to ensure accuracy and compliance. Here’s a list of things to do and avoid:

The Montana Promissory Note form shares similarities with the standard Promissory Note, which is a written promise to pay a specified amount of money to a designated person or entity. Both documents outline the borrower’s commitment to repay the loan, including the principal amount, interest rate, and repayment schedule. Additionally, both forms typically include provisions for default, allowing the lender to take specific actions if the borrower fails to meet their obligations. The fundamental structure and purpose remain consistent across various jurisdictions, ensuring that the borrower is legally bound to repay the borrowed funds.

Another document akin to the Montana Promissory Note is the Secured Promissory Note. This type of note not only includes the promise to repay but also specifies collateral that secures the loan. In the event of default, the lender has the right to seize the collateral to recover the owed amount. Like the Montana form, the Secured Promissory Note provides clarity on the terms of repayment, but it adds an extra layer of protection for the lender through the inclusion of collateral, making it a more secure option for lending.

The Loan Agreement is also comparable to the Montana Promissory Note. While a Promissory Note focuses primarily on the borrower's promise to repay, a Loan Agreement encompasses broader terms and conditions governing the entire loan transaction. This document may include details about the purpose of the loan, fees, representations, and warranties from both parties. Thus, while both documents serve the purpose of facilitating a loan, the Loan Agreement offers a more comprehensive framework for the relationship between the borrower and lender.

The Personal Loan Agreement is another document that bears resemblance to the Montana Promissory Note. This agreement outlines the terms under which an individual borrows money from another individual or institution. Similar to the Promissory Note, it specifies the loan amount, interest rate, and repayment schedule. However, the Personal Loan Agreement may also include terms regarding personal guarantees or co-signers, providing additional security for the lender. The essence of both documents is to establish a clear understanding of the repayment obligations.

Understanding the nuances of various financial agreements is crucial, as each document, such as a promissory note and a student loan agreement, serves to outline specific terms and obligations between parties. To avoid any ambiguities regarding more complex legal documents, such as a Last Will and Testament, resources like TopTemplates.info can provide guidance and clarity, ensuring that individuals can navigate these significant legal frameworks effectively.

Lastly, the Business Loan Agreement aligns closely with the Montana Promissory Note but is tailored specifically for business transactions. This document serves to formalize the terms under which a business borrows funds from a lender. It typically includes details such as the loan amount, interest rate, repayment terms, and any covenants that the business must adhere to during the loan period. Like the Promissory Note, it aims to protect the lender’s interests while ensuring that the borrower understands their obligations, thus fostering a transparent lending relationship.

After obtaining the Montana Promissory Note form, you will need to provide specific information to complete it accurately. This form will require details about the borrower, the lender, and the terms of the loan. Following these steps will help ensure that all necessary information is included.

Once you have completed the form, review all entries for accuracy. Make copies for both the borrower and lender before finalizing the agreement.

When dealing with a Montana Promissory Note, several other forms and documents may be necessary to ensure a comprehensive understanding and proper execution of the agreement. Each of these documents serves a specific purpose in the lending process.

These documents work together to create a clear framework for the loan transaction, protecting both the lender and the borrower. Ensuring all necessary forms are completed accurately will help facilitate a smooth lending process.

Understanding the Montana Promissory Note form can be challenging due to several common misconceptions. Below is a list of nine prevalent misunderstandings, along with clarifications to help illuminate the true nature of this important financial document.

This is not true. While the basic concept remains the same, each state has its own requirements and formats. The Montana Promissory Note form includes specific provisions that comply with Montana laws.

Many believe that verbal agreements suffice, but a written promissory note is crucial. A written document provides clear evidence of the terms and obligations, reducing the potential for disputes.

This is a misconception. Individuals and businesses can create promissory notes as well. The form can be used for personal loans, business transactions, or any situation where one party lends money to another.

While it is true that changes can be complicated, amendments can be made if all parties agree. It’s essential to document any changes in writing to maintain clarity.

This belief is misleading. Promissory notes can be used for any amount, whether large or small. The important factor is that both parties agree to the terms.

While a promissory note outlines the borrower's promise to repay, it does not guarantee repayment. If the borrower defaults, the lender may need to pursue legal action to recover the funds.

Interest rates can vary. The terms of the note should clearly state whether the interest rate is fixed or variable, allowing both parties to understand their obligations.

While not always required, having a witness or notarizing the document can add an extra layer of security. It helps verify the identities of the parties involved and the authenticity of the signatures.

Promissory notes typically have a specified term for repayment. Once the loan is paid off, the note should be marked as satisfied or canceled to avoid any future confusion.

Being aware of these misconceptions can help individuals navigate the process of creating and managing promissory notes more effectively. Understanding the nuances of the Montana Promissory Note form is crucial for both lenders and borrowers.

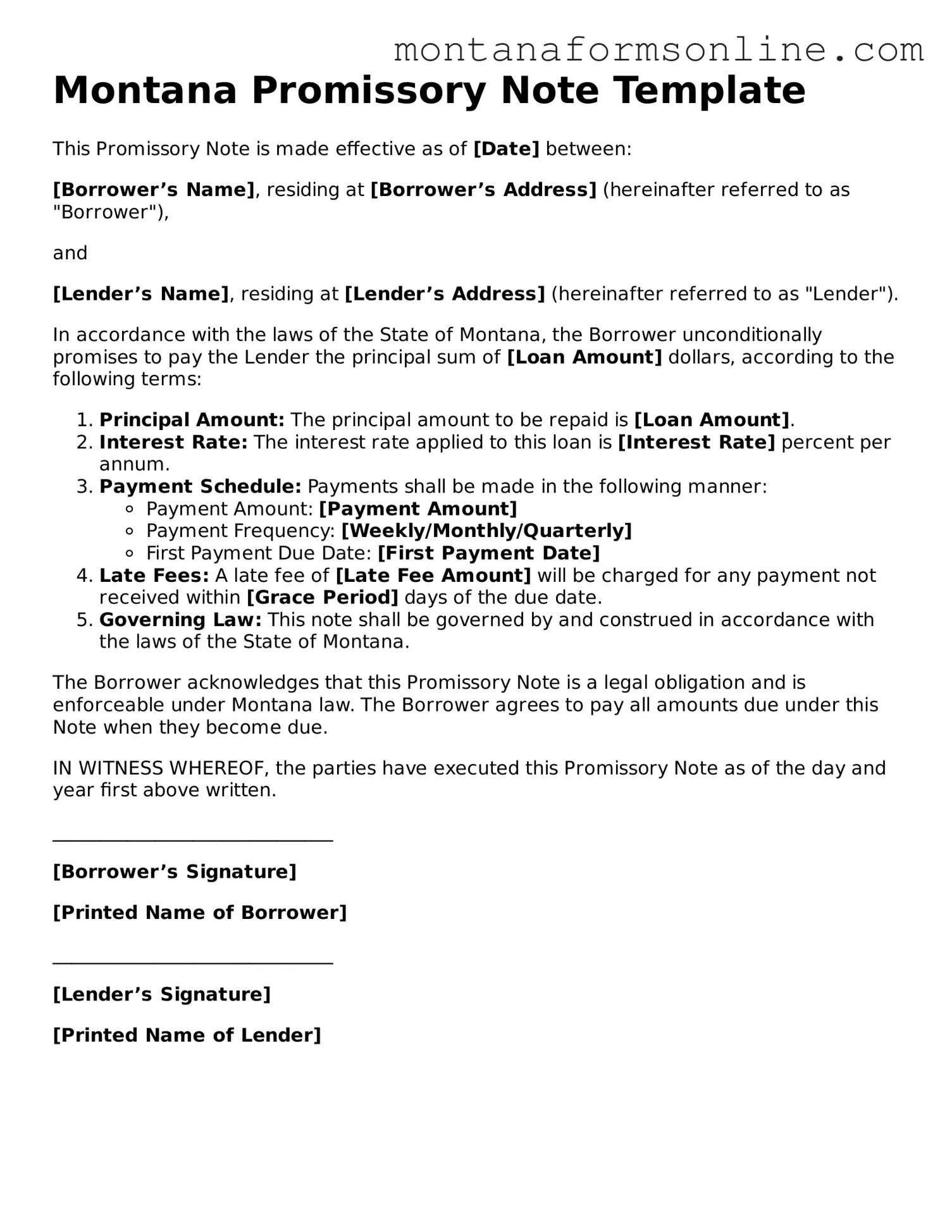

Montana Promissory Note Template

This Promissory Note is made effective as of [Date] between:

[Borrower’s Name], residing at [Borrower’s Address] (hereinafter referred to as "Borrower"),

and

[Lender’s Name], residing at [Lender’s Address] (hereinafter referred to as "Lender").

In accordance with the laws of the State of Montana, the Borrower unconditionally promises to pay the Lender the principal sum of [Loan Amount] dollars, according to the following terms:

The Borrower acknowledges that this Promissory Note is a legal obligation and is enforceable under Montana law. The Borrower agrees to pay all amounts due under this Note when they become due.

IN WITNESS WHEREOF, the parties have executed this Promissory Note as of the day and year first above written.

______________________________

[Borrower’s Signature]

[Printed Name of Borrower]

______________________________

[Lender’s Signature]

[Printed Name of Lender]

A Montana Promissory Note is a legal document that outlines a borrower's promise to repay a specific amount of money to a lender. This note includes important details such as the loan amount, interest rate, repayment schedule, and any applicable fees. It serves as a written record of the agreement between the parties involved.

This form is ideal for individuals or businesses that lend money and want to formalize the agreement. Whether you are a friend lending money to another friend or a business extending credit, using a promissory note helps protect both parties. It clearly outlines the terms of the loan, reducing the risk of misunderstandings.

When creating a Montana Promissory Note, ensure it includes the following key components:

If the borrower fails to repay the loan as agreed, the lender has the right to take legal action. To enforce the note, the lender may need to:

It’s advisable to consult with a legal professional to understand the best course of action based on your specific situation.