Blank Montana Pr 1 Form

Blank Montana Pr 1 Form

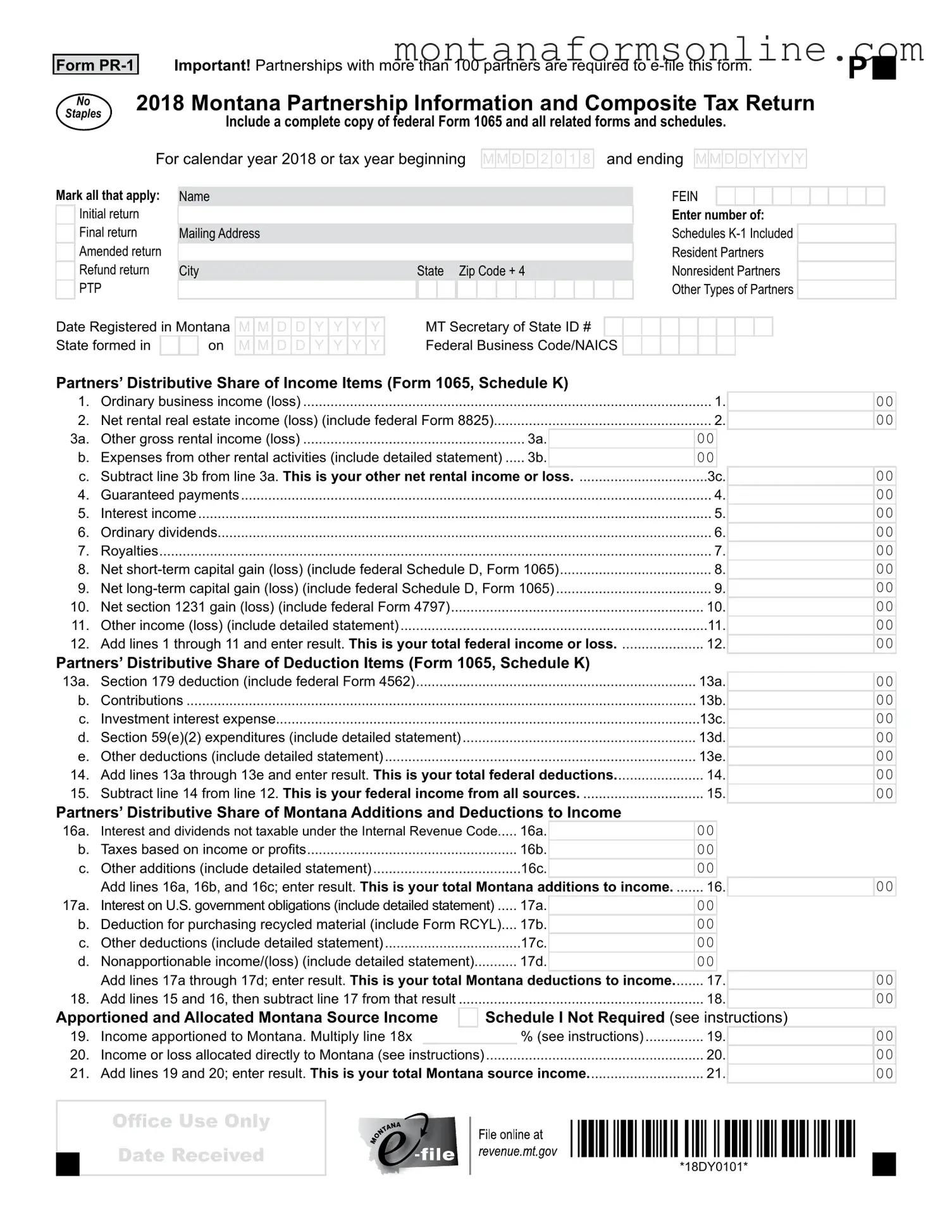

The Montana PR-1 form serves as a crucial document for partnerships operating within the state, particularly for those with more than 100 partners, as they are mandated to e-file. This form is designed to capture essential financial information about the partnership, including income, deductions, and tax liabilities, allowing for accurate reporting to the Montana Department of Revenue. Key components of the PR-1 include a requirement to attach a complete copy of federal Form 1065, along with all related schedules and forms. The form provides sections for detailing the partnership's income sources, such as ordinary business income, rental income, and capital gains, as well as deductions that can be claimed. Additionally, it requires partnerships to report their Montana-specific additions and deductions, ensuring compliance with state tax laws. The PR-1 also incorporates a calculation of any tax owed or refunds due, making it a comprehensive tool for managing partnership tax obligations in Montana. Understanding the intricacies of this form can greatly aid partnerships in navigating their tax responsibilities effectively.

Failing to mark the correct return type. Make sure to indicate whether it is an initial, final, amended, or refund return.

Not including a complete copy of federal Form 1065. This form must accompany the Montana PR-1 form along with all related schedules.

Incorrectly reporting the number of partners. Ensure you accurately count resident, nonresident, and other types of partners.

Omitting the FEIN (Federal Employer Identification Number). This number is essential for proper identification of the partnership.

Neglecting to include detailed statements for deductions or other income items. Each entry must be supported by appropriate documentation.

Failing to calculate Montana additions and deductions correctly. Review the calculations for accuracy before submitting the form.

Not providing the correct apportionment factors. These must be calculated based on the partnership's income and property in Montana.

Forgetting to sign and date the form. An unsigned form will be considered incomplete and may delay processing.

Mt Income Tax Rebate - Be prepared to explain your circumstances thoroughly to improve your chances of approval.

To ensure all parties are aware of their obligations and to minimize disputes, it is essential to utilize a comprehensive Lease Agreement form, which can be found at TopTemplates.info, as it provides a framework for understanding the key terms and conditions involved in the rental process.

Montana Post Forms - Applicants can indicate their experience with various types of equipment that may be required in the role.

When filling out the Montana PR-1 form, it is crucial to follow certain guidelines to ensure accuracy and compliance. Here are five things you should do, as well as five things you should avoid.

The Montana PR-1 form shares similarities with the IRS Form 1065, which is the U.S. Return of Partnership Income. Both forms require partnerships to report their income, deductions, and credits. The information reported on Form 1065 is critical for the preparation of the Montana PR-1, as it includes the federal partnership details that must be included with the state return. Each partner's share of income and deductions is calculated on Form 1065, which is then reflected in the Montana PR-1, ensuring consistency in reporting across federal and state levels.

For those looking to buy or sell a vehicle in California, understanding the intricacies of the process is vital. The standard vehicle purchase agreement form ensures that both parties are clear on the transaction terms, protecting their respective interests throughout the sale.

Another similar document is the Montana Schedule K-1, which details each partner's share of income, deductions, and credits from the partnership. This schedule is crucial for individual partners as it provides the information needed for their personal tax returns. Like the PR-1 form, the Schedule K-1 aligns with the federal Form 1065, ensuring that the income and deductions reported by the partnership flow through to the individual partners accurately. This connection between the two documents helps maintain transparency and consistency in tax reporting.

The IRS Form 1120-S, which is the U.S. Income Tax Return for an S Corporation, also bears similarities to the Montana PR-1 form. Both documents require the reporting of income, deductions, and credits for entities that pass income through to their owners. While the PR-1 is specific to partnerships, the Form 1120-S serves a similar purpose for S Corporations, allowing for the distribution of income to shareholders. The structure of reporting on both forms is similar, focusing on the flow-through nature of income taxation.

Lastly, the Montana Composite Income Tax Schedule is akin to the PR-1 form in its purpose of aggregating tax liabilities for partnerships with nonresident partners. This schedule allows partnerships to file a composite return on behalf of their nonresident partners, simplifying the tax process for those individuals. Both the PR-1 and the Composite Income Tax Schedule emphasize the need for accurate reporting of income and tax liabilities, ensuring that partnerships fulfill their tax obligations while providing clarity to partners regarding their respective shares.

Completing the Montana PR-1 form requires careful attention to detail. This form is essential for partnerships operating in Montana and involves reporting various financial details. Before starting, ensure you have all necessary documentation, including federal Form 1065 and related schedules. Follow these steps to accurately fill out the form.

After completing these steps, review the form for accuracy before submission. Ensure that all required documents are attached, and submit the form according to the guidelines provided by the Montana Department of Revenue. If you have questions or need assistance, consider reaching out to a tax professional.

The Montana PR-1 form serves as a vital document for partnerships operating in the state, detailing their income and tax obligations. In conjunction with this form, several other documents are commonly utilized to ensure compliance with state tax regulations. Each of these documents plays a specific role in the reporting and calculation processes associated with partnership taxation in Montana.

In summary, the Montana PR-1 form interacts with several other forms and schedules that together create a comprehensive picture of a partnership's tax responsibilities. Each document serves a unique purpose, ensuring that partnerships comply with both federal and state tax laws while maximizing their potential tax benefits.

1. E-filing is optional for all partnerships. Many believe that e-filing is optional for partnerships. However, partnerships with more than 100 partners are required to e-file the Montana PR 1 form.

2. The form does not require federal forms. Some think the PR 1 form can be submitted without including federal documentation. In fact, a complete copy of federal Form 1065 and all related forms and schedules must accompany the PR 1 form.

3. Only resident partners are reported. It's a common misconception that only resident partners need to be reported. Both resident and nonresident partners must be included in the form.

4. The form is only for calendar year filers. Many assume the PR 1 form is only for calendar year filers. It can also be used for tax years beginning on any date, not just January 1.

5. All partners must be included on the form. Some believe that all partners must be listed on the PR 1 form. However, only eligible participating partners need to be reported.

6. There are no penalties for late filing. Many think that there are no consequences for late submissions. In reality, late filing can result in penalties and interest charges.

7. The form does not require a signature. Some individuals believe they can submit the form without a signature. A signature from an officer is mandatory to validate the submission.

8. All deductions are automatically accepted. It's a misconception that all deductions claimed will be accepted without scrutiny. Each deduction must be properly documented and justified.

9. The PR 1 form is the only form needed for partnerships. Many think that submitting the PR 1 form is sufficient for all partnership tax obligations. In fact, additional forms may be required depending on the partnership’s activities.

10. Refunds are processed immediately. Some expect refunds to be processed right after filing. Refund processing can take time and is not immediate, depending on various factors.

Form |

Important! Partnerships with more than 100 partners are required to |

P |

|

No |

2018 Montana Partnership Information and Composite Tax Return |

|

|

|

|

|

|

Staples |

Include a complete copy of federal Form 1065 and all related forms and schedules. |

|

|

|

|

|

For calendar year 2018 or tax year beginning

M M

M D

D D

D 2 0

2 0  1 8

1 8

and ending

M M D D

D D Y

Y Y

Y Y

Y Y

Y

Mark all that apply:

Initial return Final return Amended return Refund return

PTP

Name

Mailing Address

City |

State Zip Code + 4 |

FEIN

Enter number of:

Schedules

Resident Partners

Nonresident Partners

Other Types of Partners

Date Registered in Montana |

M |

M |

D |

D |

Y |

Y |

Y |

Y |

MT Secretary of State ID # |

|

|

|

|

|

|

|

|

|

|||

State formed in |

|

|

on |

M |

M |

D |

D |

Y |

Y |

Y |

Y |

Federal Business Code/NAICS |

|

|

|

|

|

|

|

|

|

Partners’ Distributive Share of Income Items (Form 1065, Schedule K) |

|

|||

1. |

Ordinary business income (loss) |

|

1. |

|

2. |

Net rental real estate income (loss) (include federal Form 8825) |

2. |

||

3a. |

Other gross rental income (loss) |

3a. |

00 |

|

b. |

Expenses from other rental activities (include detailed statement) |

3b. |

00 |

|

c. |

Subtract line 3b from line 3a. This is your other net rental income or loss |

3c. |

||

4. |

Guaranteed payments |

|

4. |

|

5. |

Interest income |

|

5. |

|

6. |

Ordinary dividends |

|

6. |

|

7. |

Royalties |

|

7. |

|

8. |

Net |

8. |

||

9. |

Net |

9. |

||

10. |

Net section 1231 gain (loss) (include federal Form 4797) |

|

10. |

|

11. |

Other income (loss) (include detailed statement) |

|

11. |

|

12. |

Add lines 1 through 11 and enter result. This is your total federal income or loss |

12. |

||

Partners’ Distributive Share of Deduction Items (Form 1065, Schedule K) |

|

|||

13a. |

Section 179 deduction (include federal Form 4562) |

|

13a. |

|

b. |

Contributions |

|

13b. |

|

c. |

Investment interest expense |

|

13c. |

|

d. |

Section 59(e)(2) expenditures (include detailed statement) |

|

13d. |

|

e. |

Other deductions (include detailed statement) |

|

13e. |

|

14. |

Add lines 13a through 13e and enter result. This is your total federal deductions |

14. |

||

15. |

Subtract line 14 from line 12. This is your federal income from all sources |

15. |

||

Partners’ Distributive Share of Montana Additions and Deductions to Income |

|

|||

16a. |

Interest and dividends not taxable under the Internal Revenue Code |

16a. |

00 |

|

b. |

Taxes based on income or profits |

16b. |

00 |

|

c. |

Other additions (include detailed statement) |

16c. |

00 |

|

|

Add lines 16a, 16b, and 16c; enter result. This is your total Montana additions to income |

16. |

||

17a. |

Interest on U.S. government obligations (include detailed statement) |

17a. |

00 |

|

b. |

Deduction for purchasing recycled material (include Form RCYL).... |

17b. |

00 |

|

c. |

Other deductions (include detailed statement) |

17c. |

00 |

|

d. |

Nonapportionable income/(loss) (include detailed statement) |

17d. |

00 |

|

|

Add lines 17a through 17d; enter result. This is your total Montana deductions to income |

17. |

||

18. |

Add lines 15 and 16, then subtract line 17 from that result |

|

18. |

|

Apportioned and Allocated Montana Source Income |

Schedule I Not Required (see instructions) |

|||

19. |

Income apportioned to Montana. Multiply line 18x |

|

% (see instructions) |

19. |

20. |

Income or loss allocated directly to Montana (see instructions) |

........................................................ |

20. |

|

21. |

Add lines 19 and 20; enter result. This is your total Montana source income |

21. |

||

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

Office Use Only Date Received

*18DY0101*

*18DY0101*

*18DY0101*

Form |

FEIN |

|

|

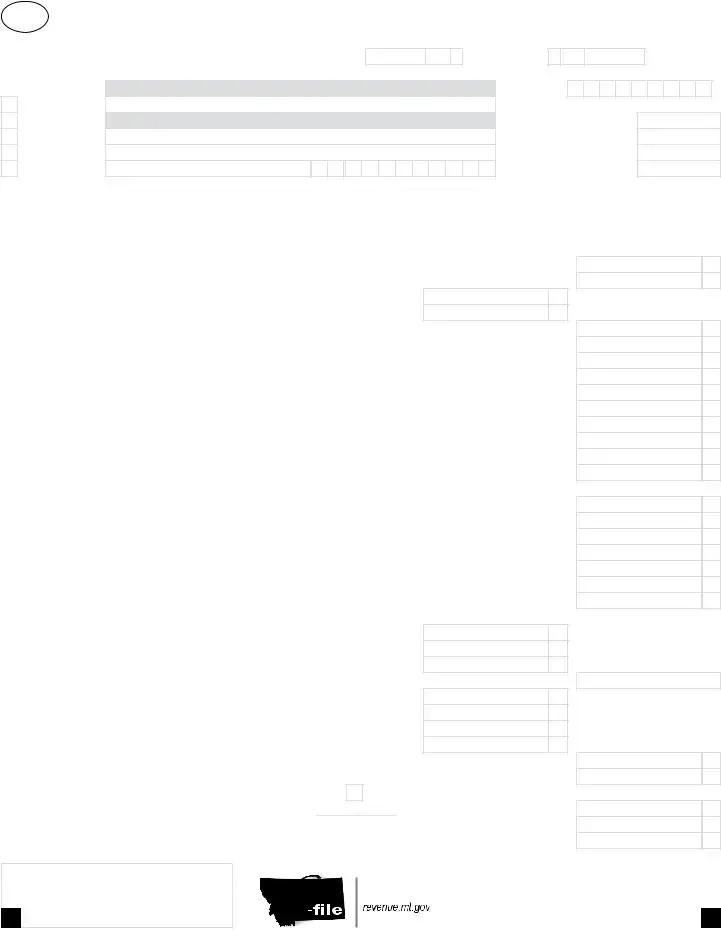

Calculation of Amount Owed or Refund |

|

|

|

22. |

Enter your Montana total composite tax from Schedule IV, column H |

............................................... |

22. |

23. |

Enter the sum of |

23. |

|

Withholding |

|

|

|

24 a. Total Montana mineral royalty tax withheld on your behalf (see instructions) 24a. |

00 |

||

|

b. Mineral royalty tax withheld distributed to partners |

24b. |

00 |

|

c. Subtract 24b from 24a. Montana mineral royalty tax withheld attributable to partnership |

24c. |

|

25 a. Total Montana |

00 |

||

|

b. Montana |

25b. |

00 |

|

c. Subtract line 25b from 25a. Montana |

25c. |

|

26. |

Add lines 24c and 25c. This is the total withholding payments attributable to partnership |

26. |

|

Return Payments

00

00

00

00

00

00

27 a. |

2017 overpayment applied to 2018 |

27a. |

00 |

b. |

2018 estimated payments |

27b. |

00 |

c. |

2018 extension payment |

27c. |

00 |

d. |

For amended returns |

27d. |

00 |

e. |

For amended returns |

00 |

|

f. |

Add lines 27a through 27d, then subtract line 27e. This is your total return payments |

27f. |

|

28. Add lines 22 and 23, then subtract lines 26 and 27f. This is your amount due or (overpaid) |

28. |

||

Penalties and Interest (see instructions) |

|

|

|

29 a. Partnership information return late filing penalty |

29a. |

00 |

|

b. Interest on underpayment of estimated composite tax |

29b. |

00 |

|

c. Composite income tax return late filing penalty |

29c. |

00 |

|

d. Late payment penalty |

29d. |

00 |

|

e. Interest |

29e. |

00 |

|

f. |

Add lines 29a through 29e. This is your total penalties and interest |

29f. |

|

Amount Owed or Refund |

|

|

|

30. Add lines 28 and 29f |

30. |

||

31. If line 30 results in an amount due, enter it here. This is the amount you owe |

31. |

||

00

00

00

00

00

00

Pay online at revenue.mt.gov. If writing a check, make it payable to MONTANA DEPARTMENT OF REVENUE.

32.If line 30 results in an overpayment, enter it here. This is your overpayment. Enter as a positive number. 32.

33.Enter the amount from line 32 that you want applied to your 2019 composite

.............................................................................................estimated tax |

33. |

|

00 |

|

34. Subtract line 33 from line 32 and enter the amount here. This is your refund |

................................. |

34. |

||

00

00

00

00

Direct Deposit |

1. RTN# |

|

|

|

|

|

|

|

|

|

2. ACCT# |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Your Refund |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Complete 1, 2, 3 and 4 |

3. |

If using direct deposit, you are required to mark one box. ► |

|

|

Checking |

|

|

Savings |

|

|

|

|

|

|

|

|

||||||||||||||||||||

(see instructions). |

4. |

Is this refund going to an account that is located outside of the |

United States or its territories? |

|

|

Yes |

|

No |

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of false swearing, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete.

Signature of Officer |

Date |

Printed Name and Title |

|

Telephone Number |

||||||||||||||||||||

|

X ____________________________________________ |

|

M |

M |

D |

D |

Y |

Y |

Y |

Y |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Print/Type Preparer’s Name

Firm’s Name

Preparer’s SignatureDate

____________________________________ |

M M D D Y Y Y Y |

Firm’s Address |

Telephone Number |

PTIN

Firm’s FEIN |

May the DOR discuss this tax return with your tax preparer?  Yes

Yes

No

No

*18DY0201*

*18DY0201*

Form

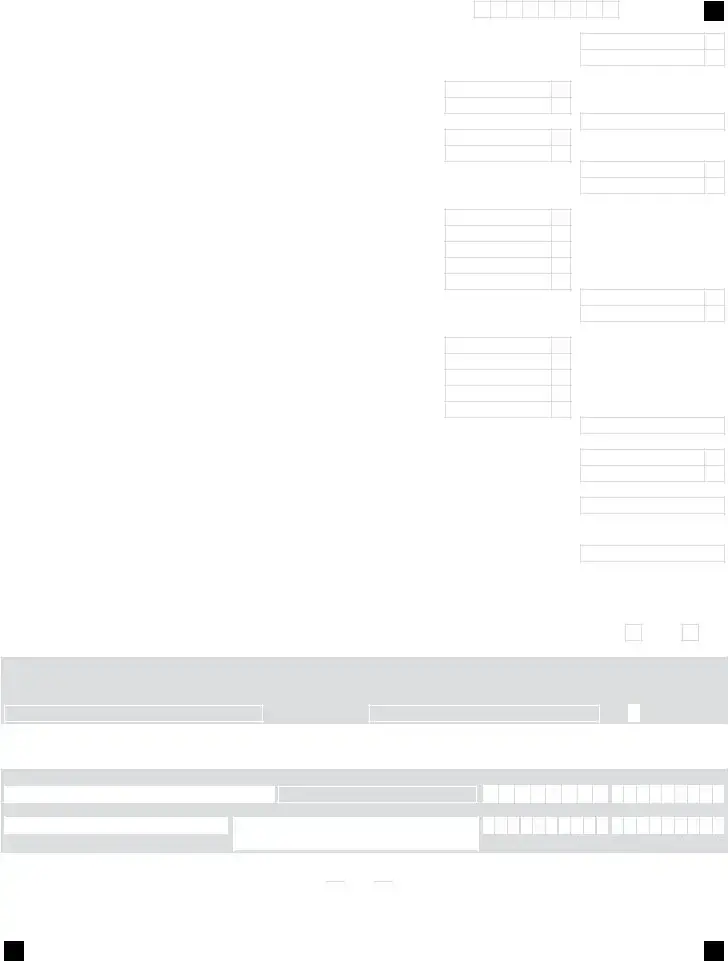

Schedule I - Apportionment Factors for Multistate Partnerships

Enter amounts in columns A and B. Enter percentages in column C. |

A. Everywhere |

B. Montana. |

C. Factor |

1.Property Factor: Use average value for real and tangible personal property.

1a. |

.............................................................................................Land |

|

|

00 |

|

|

|

|

|

00 |

|

|

1b. |

......................................................................................Buildings |

|

|

00 |

|

|

|

|

|

00 |

|

|

....................................................................................1c. Machinery |

|

|

00 |

|

|

|

|

|

00 |

|

||

1d. |

Equipment |

1d. |

|

|

00 |

|

|

|

|

|

00 |

|

1e. |

...................................................................Furniture and fixtures |

|

|

00 |

|

|

|

|

|

00 |

|

|

1f. |

.........................................................Leases and leased property |

|

|

00 |

|

|

|

|

|

00 |

|

|

1g. |

...................................................................................Inventories |

|

|

00 |

|

|

|

|

|

00 |

|

|

1h. |

........................................................................Depletable assets |

|

|

00 |

|

|

|

|

|

00 |

|

|

1i. |

........................................................................Supplies and other |

|

|

00 |

|

|

|

|

|

00 |

|

|

..................1j. Property of foreign subs included in combined group |

|

|

00 |

|

|

|

|

|

00 |

|

||

....1k. Property of unconsolidated subs included in combined group |

|

|

00 |

|

|

|

|

|

00 |

|

||

1l. |

.....Property of |

|

|

00 |

|

|

|

|

|

00 |

|

|

............................1m.Multiply amount of rents by 8 and enter result |

1m. |

|

|

00 |

|

|

|

|

|

00 |

|

|

....................................Total Property Value add lines 1a through 1m |

|

|

00 |

|

|

|

|

|

00 |

|

||

Divide the total in column B by the total in column A. Multiply the result |

by 100. This is your |

property |

factor |

1. |

|

|

|

|||||

2. Payroll Factor: |

|

|

|

|

|

|

|

|

|

|

|

|

2a. |

.............................................................Compensation of officers |

|

|

00 |

|

|

|

|

|

00 |

|

|

2b. |

.....................................................................Salaries and wages |

|

|

00 |

|

|

|

|

|

00 |

|

|

|

Payroll included in: |

|

|

|

|

|

|

|

|

|

|

|

2c. |

.....................................................................Costs of goods sold |

|

|

00 |

|

|

|

|

|

00 |

|

|

2d. |

..................................................Other expenses and deductions |

|

|

00 |

|

|

|

|

|

00 |

|

|

2e. |

....................Payroll of foreign subs included in combined group |

|

|

00 |

|

|

|

|

|

00 |

|

|

2f. |

........Payroll of unconsolidated subs included in combined group |

|

|

00 |

|

|

|

|

|

00 |

|

|

2g. |

......Payroll of |

|

|

00 |

|

|

|

|

|

00 |

|

|

........................................Total Payroll Value add lines 2a through 2g |

|

|

00 |

|

|

|

|

|

00 |

|

||

Divide the total in column B by the total in column A. Multiply the result |

by 100. This is your payroll |

|

factor |

2. |

|

|

|

|||||

3. Gross Receipts Factor: |

|

|

|

|

|

|

|

|

|

|

|

|

3a. |

.............................Gross Receipts, less returns and allowances |

3a. |

|

|

00 |

|

|

|

|

|

|

|

3b. |

Receipts delivered or shipped to Montana purchasers: |

|

|

|

|

|

|

|

|

|

|

|

|

.................................................................................(1) Shipped from outside Montana |

|

3b.(1) |

|

|

00 |

|

|||||

|

...................................................................................(2) Shipped from within Montana |

|

3b.(2) |

|

|

00 |

|

|||||

3c. Receipts shipped from Montana to: |

|

|

|

|

|

|

|

|

|

|

|

|

|

........................................................................................(1) United States government |

|

3c.(1) |

|

|

|

|

00 |

|

|||

|

..........................................(2) Purchasers in a state where the taxpayer is not taxable |

|

|

|

|

00 |

|

|||||

3d. |

......................Receipts other than receipts of tangible personal property (e.g. service income) |

3d. |

|

|

|

|

00 |

|

||||

3e. |

........Net gains reported on federal Schedule D and Form 4797 |

3e. |

|

|

00 |

|

|

|

|

|

00 |

|

3f. |

....................Other gross receipts (rents, royalties, interest, etc.) |

|

|

00 |

|

|

|

00 |

|

|||

3g. |

................Receipts of foreign subs included in combined group |

3g. |

|

|

00 |

|

|

|

00 |

|

||

3h. |

...Receipts of unconsolidated subs included in combined group |

3h. |

|

|

00 |

|

|

|

00 |

|

||

3i. Receipts |

|

|

|

|

|

|

|

|

|

|

|

|

|

. ................................................included in combined group |

|

|

00 |

|

|

|

|

|

00 |

|

|

3j. |

............................................Less: All intercompany transactions |

|

|

00 |

|

|

|

|

|

00 |

|

|

......................................Total Receipts Value add lines 3a through 3j |

|

|

00 |

|

|

|

|

|

00 |

|

||

Divide the total in column B by the total in column A. Multiply the result |

by 100. This is your receipts |

factor |

3. |

|

|

|

|

|||||

.................................................4. Add the percentages on lines 1, 2, and 3 in column C. This is the sum of your factors |

|

|

|

4. |

|

|

|

|

||||

5.Divide the percentage on line 4 by the number of factors included in the calculation of line 4. If a property,payroll

or receipts factor is 0%, it is included in the calculation of line 4 if there’s is a value in column A (see instructions). |

|

Enter the result here and also on page 1, line 19 of this form. This is your apportionment factor |

5. |

%

%

%

%

%

*18DY0301*

*18DY0301*

Form

|

Schedule II - Montana Partnership Tax Credits |

|

|

Type of Credit |

Amount of Credit |

|

|

1. |

Dependent Care Assistance Credit |

|

|

|

|

|

|

|

|

|

include Form DCAC |

||||

2. |

College Contribution Credit |

|

|

|

|

|

|

|

|

|

|

include Form CC |

|||

3. |

Health Insurance for Uninsured Montanans Credit |

|

|

|

|

|

|

|

|

|

|

include Form HI |

|||

4. |

Recycle Credit |

|

|

|

|

|

|

|

|

|

include Form RCYL |

||||

5. |

Alternative Energy Production Credit |

|

|

|

|

|

|

|

|

|

include Form AEPC |

||||

6. |

Contractor’s Gross Receipts Tax Credit. If multiple CGR accounts, mark here. |

||||||||||||||

|

CGR Account ID: |

|

|

|

|

|

|

|

|

|

|

C |

G |

R |

|

7. |

.......................................................................................................Alternative Fuel Credit |

|

|

|

|

|

|

|

|

|

|

|

include Form AFCR |

||

8. |

Infrastructure User Fee Credit |

|

|

|

|

|

|

|

|

|

include Form IUFC |

||||

9. |

Historic Property Preservation Credit |

|

|

|

|

|

|

|

include federal Form 3468 |

||||||

10. |

Mineral and Coal Exploration Incentive Credit |

|

include Forms |

||||||||||||

11. |

Empowerment Zone Credit |

|

|

|

|

|

|

|

|

|

|

|

|

||

12. |

Biodiesel Blending and Storage Credit |

|

|

|

|

|

|

|

|

|

include Form BBSC |

||||

13.Innovative Educational Program Credit.............................................................................................................

14.Student Scholarship Organization Credit ..........................................................................................................

15. Emergency Lodging Credit |

include Form ELC |

16.Unlocking Public Lands Credit...........................................................................................................................

17.Apprenticeship Tax Credit..................................................................................................................................

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

Type of Credit Recapture |

Amount of Credit |

|

|

|

Recapture |

18. |

Historic Property Preservation Credit Recapture |

00 |

19. |

Film Production Credit Recapture |

00 |

20. |

Biodiesel Blending and Storage Credit Recapture |

00 |

21. |

Oilseed Crushing and Biodiesel/Biolubricant Production Credit Recapture |

00 |

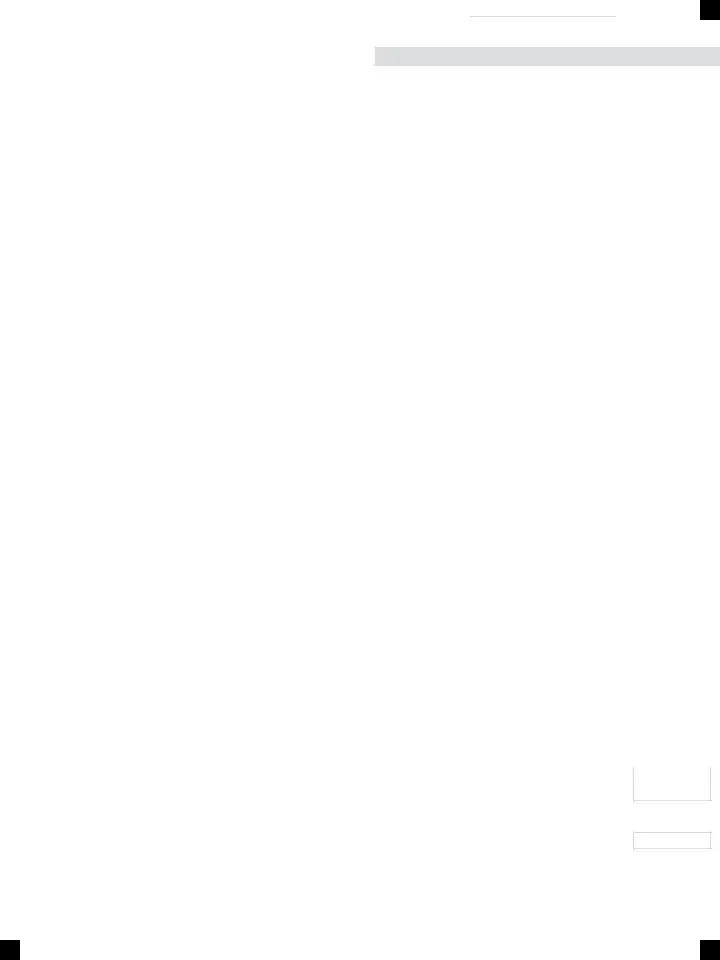

When attributing any credit or credit recapture from a partnership to its partners, use the same proportion the partnership used to report each partner’s income or loss for Montana tax purposes. Include a detailed breakdown that shows each partner’s share of the credit or credit recapture.

Use Montana Schedule

*18DY0401*

*18DY0401*

Form |

FEIN |

|

|

|

|

|

|

|

|

|

|

|

|

Schedule IV – Montana Partnership Composite Income Tax Schedule |

|

|

|

|

|

|

|

|

|

||

Part I. Eligible Participating Partners

Enter the number of eligible participating partners. See instructions for more information about eligible participating partners.

Part II. Composite Tax Ratio |

1 |

|

2 |

3 |

|

Use the amount in column 3 |

Enter the amount from |

Enter the amount from |

|

Divide column 2 by |

|

to complete the calculation |

page 1, line 15 |

page 1, line 21 |

|

column 1 |

|

|

Do not enter more than |

||||

in column H below. |

of this form. |

of this form. |

|

1.000000 |

|

|

|

00 |

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Part III. Enter below in columns A through H the required information and amounts for each eligible participating partner. |

|

|

|

|

|||||||||||

|

|

A |

B |

C |

D |

E |

F |

G |

H |

||||||

|

|

|

Social security |

|

|

|

|

|

|

Montana taxable |

|

|

Montana composite |

||

|

|

|

number or |

Partner’s share of |

|

|

|

|

Enter the appropriate |

income tax. Multiply |

|||||

|

|

Name |

Standard |

Exemption |

income – Subtract |

||||||||||

|

|

federal employer |

federal income from |

deduction |

$2,440 |

columns D and E |

tax from the tax table |

column G times |

|||||||

|

|

|

identification |

entity |

below. |

composite tax ratio |

|||||||||

|

|

|

|

|

|

|

from column C. |

||||||||

|

|

|

number |

|

|

|

|

|

|

|

|

from Part II. |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

1. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

2. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

3. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

4. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

5. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

6. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

7. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

8. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

9. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

10. |

|

|

|

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

11. |

|

Enter the total composite tax from all additional |

pages, if used |

|

|

|

|

|

|

|

|

|

11. |

|

00 |

|

|

|

|

Add column H, lines 1 through 11. This is your total composite income tax liability. |

|

00 |

|||||||||

|

|

|

Transfer the amounts from column H to each partner’s Montana Schedule |

|

|

||||||||||

*18DY0501*

*18DY0501*

If additional space is needed, make copies of this page. Include all additional pages from line 11 with the tax return.

If Your Taxable |

But Not More Than |

Multiply Your |

And Subtract |

This Is Your |

|

|

Income Is More Than |

Taxable Income By |

Tax |

|

|

||

|

|

|

|

|

|

|

$0 |

$3,000 |

1% (0.010) |

$0 |

|

|

|

$3,000 |

$5,200 |

2% (0.020) |

$30 |

|

|

|

$5,200 |

$8,000 |

3% (0.030) |

$82 |

|

|

|

$8,000 |

$10,800 |

4% (0.040) |

$162 |

|

|

|

$10,800 |

$13,900 |

5% (0.050) |

$270 |

|

|

|

$13,900 |

$17,900 |

6% (0.060) |

$409 |

|

|

|

|

More Than $17,900 |

6.9% (0.069) |

$570 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form

Schedule VI – Reporting of Special Transactions

Complete Schedule VI only if your partnership filed any of the federal income tax forms described below. Mark the appropriate box indicating which form(s) you filed with the Internal Revenue Service for this tax year. If your answer is “Yes” to one or more of these forms, you need to include a complete copy of your federal tax return Form 1065.

|

1. |

The partnership filed federal Form 8918 – Material Advisor Disclosure Statement with the Internal |

|

|

|

|

Revenue Service. |

Yes |

|

|

|

Material advisors to any reportable transactions must file Form 8918. |

|

|

|

2. |

The partnership filed federal Form 8824 – |

Yes |

|

|

|

NOTE: Mark the box if your |

||

|

|

|

|

|

|

|

have to report a |

|

|

|

|

Use Form 8824 to report each exchange of business or investment property for property of a like- |

|

|

|

|

kind. |

|

|

|

3. |

The partnership filed federal Form 8865 – Return of U.S. Persons With Respect to Certain |

|

|

|

|

Foreign Partnerships with the Internal Revenue Service. |

Yes |

|

|

|

Use Form 8865 to report the information required under 26 USC 6038 (reporting with respect to |

|

|

|

|

controlled foreign partnerships), Section 6038B (reporting of transfers to foreign partnerships) or |

|

|

|

|

Section 6046A (reporting of acquisitions, dispositions and changes in foreign partnership interest). |

|

|

|

4. |

The partnership filed federal Form 8886 – Reportable Transaction Disclosure Statement with the |

|

|

|

|

Internal Revenue Service. |

Yes |

|

|

|

Use Form 8886 to disclose information for each reportable transaction in which you participated. |

|

|

Complete this section if you made a disbursement to a related party.

5.During this tax year, the partnership made payments to one or more related parties

(excluding salary compensation) that exceed $100,000 per recipient.

If you answer “Yes” to this question, please provide the name and federal employer identification number of each related party below and the amount that you paid to each related party:

Name |

|

|

|

|

FEIN |

Amount of Payment |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Yes

*18DY0601*

*18DY0601*

The Montana PR-1 form is primarily used by partnerships to report their income, deductions, and tax liabilities to the state of Montana. This form includes detailed information about the partnership’s financial activities for the tax year, including distributions to partners, income sources, and applicable deductions. Partnerships with more than 100 partners are required to e-file this form.

To complete the PR-1 form, you will need the following information:

If your partnership has more than 100 partners, you are required to e-file the PR-1 form. For partnerships with 100 or fewer partners, e-filing is not mandatory but may still be an option. Always check the latest guidelines from the Montana Department of Revenue to ensure compliance.

Submitting the PR-1 form late can result in penalties and interest. The Montana Department of Revenue imposes a late filing penalty on partnerships that do not file on time. Additionally, interest may accrue on any unpaid taxes. To avoid these consequences, ensure that you file the form by the due date, which is typically the 15th day of the fourth month following the end of the tax year.

You can pay any taxes owed on the PR-1 form online through the Montana Department of Revenue's website. If you prefer to pay by check, make it payable to the Montana Department of Revenue. Ensure that you include your FEIN and the tax year on the check to avoid processing delays.