Blank Montana Apls101F Form

Blank Montana Apls101F Form

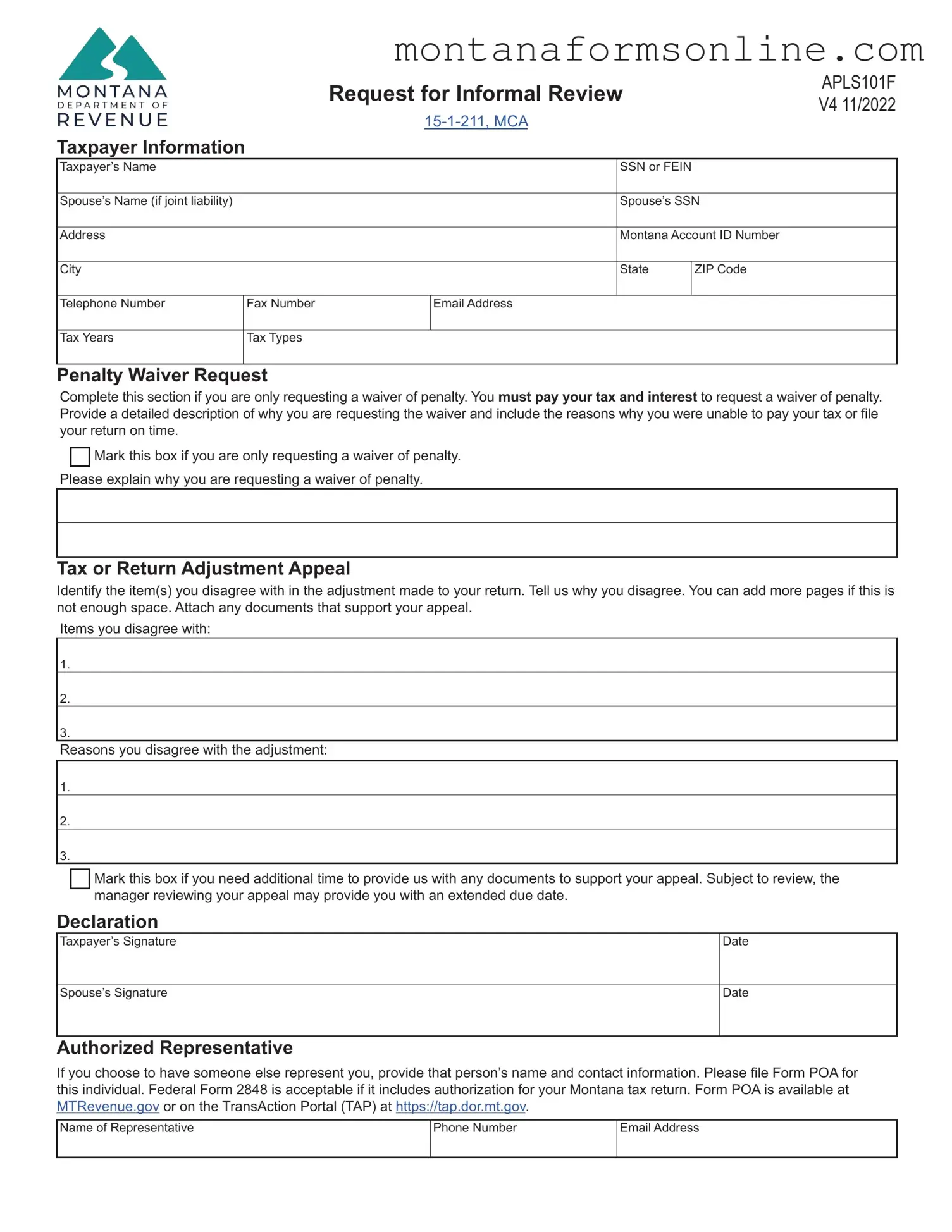

The Montana Apls101F form serves as a crucial tool for taxpayers seeking to address discrepancies in their tax assessments or to request a waiver of penalties associated with late payments. This form can be utilized to formally request an informal review of a Notice of Assessment (NOA), which is issued when the Montana Department of Revenue makes adjustments to a taxpayer's return. Within this form, individuals must provide essential information, including their name, Social Security Number (SSN) or Federal Employer Identification Number (FEIN), and details about their tax situation. Taxpayers can also specify the tax years and types involved, along with a description of the reasons for their waiver request or disagreement with the adjustments made. The form allows for the inclusion of supporting documents and gives the option to extend the due date for submitting additional evidence. Additionally, it requires signatures from both the taxpayer and their spouse, if applicable, ensuring that all parties are informed and in agreement. For those needing representation, the form provides space to designate an authorized representative, streamlining communication with the Department of Revenue. Overall, the Apls101F form is designed to facilitate a transparent and fair process for taxpayers navigating the complexities of tax assessments in Montana.

Neglecting to provide complete taxpayer information: It is essential to fill in all required fields, including your name, Social Security Number (SSN) or Federal Employer Identification Number (FEIN), and contact details. Missing information can delay the review process.

Forgetting to include spouse details: If you are filing jointly, ensure that you include your spouse’s name and SSN. Omitting this information can lead to complications in processing your request.

Not specifying the tax years and types: Clearly indicate the tax years and types you are addressing. This helps the department understand the context of your appeal or waiver request.

Failing to pay tax and interest before requesting a penalty waiver: Remember, you must pay your tax and interest to request a waiver of penalty. Ignoring this requirement can result in automatic denial of your waiver request.

Providing insufficient reasons for penalty waiver: When requesting a waiver, include a detailed explanation of why you were unable to pay on time. Vague reasons may not be considered valid.

Overlooking the appeal process deadline: It’s crucial to submit your request for an informal review within 30 days of receiving your Notice of Assessment (NOA). Missing this deadline can limit your options for appeal.

Neglecting to attach supporting documents: If you disagree with an adjustment, provide any relevant documents that support your position. Failing to do so may weaken your appeal.

Marking the wrong boxes: Carefully read the instructions and ensure you mark the appropriate boxes on the form. Incorrect markings can lead to misunderstandings about your request.

Not including an authorized representative's information: If you wish for someone else to represent you, be sure to provide their name and contact information. Additionally, file the necessary Form POA to authorize them.

Montana Tax Id - Informative instructions are available on the reverse of the form to guide you.

The California Articles of Incorporation form is essential for officially registering a corporation with the state, marking the beginning of its legal existence. This vital step is necessary for any business planning to establish itself as a corporation within California. It includes important details such as the corporation's name, purpose, and information about its shares and initial agents, which can be further explored at onlinelawdocs.com/california-articles-of-incorporation.

What Is Tax Form 540 2ez - Direct deposit requires routing and account numbers to expedite refunds.

When filling out the Montana Apls101F form, it is essential to follow specific guidelines to ensure your request is processed smoothly. Here are seven things you should and shouldn't do:

By adhering to these guidelines, you can enhance the likelihood of a favorable outcome in your appeal process.

The Montana Form APLS101F is similar to the IRS Form 843, which is used to request a refund or abatement of certain taxes. Both forms allow taxpayers to challenge tax assessments or penalties they believe are incorrect. While the APLS101F specifically addresses informal reviews and penalty waivers within Montana, Form 843 serves a broader purpose at the federal level. Taxpayers can provide reasons for their requests and attach supporting documentation in both cases, ensuring that their appeals are well-documented and justified.

Understanding the nuances of tax forms and appeals can be daunting for many taxpayers, but resources are available to guide them through the process. For instance, it's important to recognize the significance of documenting one's circumstances clearly and accurately, particularly when engaging with forms like the Montana APLS101F or any equivalent. Additionally, utilizing specialized templates can further simplify the journey; one such platform is TopTemplates.info, which provides essential resources to assist individuals in navigating legal documentation effectively.

Another comparable document is the IRS Form 9465, which is used to request a monthly installment plan for paying taxes owed. Like the APLS101F, this form addresses financial hardships and offers a way for taxpayers to manage their obligations. Both forms require detailed information about the taxpayer's financial situation and the reasons for their requests. While the APLS101F focuses on informal reviews and waivers, Form 9465 specifically addresses payment arrangements, making it a vital tool for those struggling to meet tax deadlines.

The Montana Form APLS101F also resembles the IRS Form 1040X, which is the amended U.S. Individual Income Tax Return. Both forms allow taxpayers to correct errors or discrepancies in previously filed returns. The APLS101F provides a mechanism for appealing decisions made by the Montana Department of Revenue, while Form 1040X allows taxpayers to amend their federal tax returns. Both processes require clear explanations of the changes being made and supporting documentation to substantiate the claims.

Additionally, the Montana Form APLS101F is similar to the IRS Form 12203, which is used to request a collection due process hearing. Both forms serve as avenues for taxpayers to contest decisions made by tax authorities. The APLS101F focuses on informal reviews and penalty waivers, while Form 12203 allows taxpayers to appeal collection actions. Each form requires the taxpayer to explain their case and provide supporting evidence to facilitate a fair review.

Another related document is the Montana Form APLS102F, which is the Notice of Referral to the Office of Dispute Resolution. This form is used when a taxpayer wishes to escalate their appeal after receiving a decision on their APLS101F request. Both forms are integral to the appeal process in Montana, allowing taxpayers to pursue their concerns through different levels of review. The APLS102F specifically facilitates a further examination of disputes, while the APLS101F initiates the informal review process.

Lastly, the IRS Form 2848, Power of Attorney and Declaration of Representative, is relevant as it allows taxpayers to authorize someone to represent them before the IRS. This form aligns with the APLS101F's section on authorized representatives, where taxpayers can designate someone to handle their appeal. Both forms ensure that representatives can communicate effectively with tax authorities, streamlining the process for taxpayers who may need assistance navigating complex tax issues.

Filling out the Montana APLS101F form requires careful attention to detail. This form is essential for those seeking an informal review of a Notice of Assessment or requesting a waiver of penalty. To ensure that the process goes smoothly, follow these steps closely.

The Montana APLS101F form is essential for requesting an informal review of a Notice of Assessment or a penalty waiver. However, it is often used alongside other important documents that can help support your case or clarify your situation. Here are five commonly associated forms and documents:

Understanding these forms and how they relate to the APLS101F can significantly enhance your ability to navigate the informal review process effectively. Always ensure that you have the correct documentation ready to support your requests and appeals.

This is not true. You must submit the APLS101F form within 30 days of receiving your Notice of Assessment (NOA). If you miss this deadline, it may be considered an admission of agreement with the adjustment, unless you can demonstrate reasonable cause for your delay.

This is incorrect. To request a waiver of penalty, you must first pay your tax and interest. The form allows you to explain why you were unable to pay on time, but payment is a prerequisite for the waiver request.

While the form is primarily used for disputes regarding tax assessments, it also serves as a request for a waiver of penalty. This dual purpose means that even if you agree with the assessment, you may still use the form to seek relief from penalties.

This is misleading. To strengthen your appeal, it is crucial to attach any relevant documents that support your case. Providing thorough information can significantly impact the outcome of your review.

This assumption is false. After submitting the form, a manager will review your appeal and determine the outcome. You will receive a response within 30 days, which may or may not agree with your position. Understanding this process can help manage expectations.

|

|

|

Request for Informal Review |

APLS101F |

||

|

|

|

V4 11/2022 |

|||

|

|

|

|

|

|

|

|

|

|

|

|||

Taxpayer Information |

|

|

|

|

|

|

Taxpayer’s Name |

|

|

|

SSN or FEIN |

|

|

|

|

|

|

|

|

|

Spouse’s Name (if joint liability) |

|

|

|

Spouse’s SSN |

||

|

|

|

|

|

|

|

Address |

|

|

|

Montana Account ID Number |

||

|

|

|

|

|

|

|

City |

|

|

|

State |

ZIP Code |

|

|

|

|

|

|

|

|

Telephone Number |

|

Fax Number |

|

Email Address |

|

|

|

|

|

|

|

|

|

Tax Years |

|

Tax Types |

|

|

|

|

|

|

|

|

|

|

|

Penalty Waiver Request

Complete this section if you are only requesting a waiver of penalty. You must pay your tax and interest to request a waiver of penalty.

Provide a detailed description of why you are requesting the waiver and include the reasons why you were unable to pay your tax or file your return on time.

Mark this box if you are only requesting a waiver of penalty.

Please explain why you are requesting a waiver of penalty.

Tax or Return Adjustment Appeal

Identify the item(s) you disagree with in the adjustment made to your return. Tell us why you disagree. You can add more pages if this is not enough space. Attach any documents that support your appeal.

Items you disagree with:

1.

2.

3.

Reasons you disagree with the adjustment:

1.

2.

3.

Mark this box if you need additional time to provide us with any documents to support your appeal. Subject to review, the manager reviewing your appeal may provide you with an extended due date.

Declaration

Taxpayer’s Signature

Spouse’s Signature

Date

Date

Authorized Representative

If you choose to have someone else represent you, provide that person’s name and contact information. Please file Form POA for this individual. Federal Form 2848 is acceptable if it includes authorization for your Montana tax return. Form POA is available at

MTRevenue.gov or on the TransAction Portal (TAP) at https://tap.dor.mt.gov.

Name of Representative

Phone Number

Email Address

Request for Informal Review Instructions

Purpose of this form

You may use this form to request an informal review of a

Notice of Assessment (NOA) or to request a waiver of penalty. An NOA is the first notice that the department will send you

if we adjust your return, change the amount you owe, or reduce your refund. It may come to you in the form of an audit determination letter, a return adjustment notice, or as

your first bill. An informal review is a written request to have a

department manager review the determination outlined in your

NOA. If you disagree with the NOA, use this form to begin

the informal review process. You must submit a request for informal review within 45 days of the date on your NOA.

A Statement of Account (SOA) is a bill that you will receive

if you do not request an informal review or pay the balance due showing on your NOA. You will continue to receive an SOA on a monthly basis until you pay the amount on the bill. If you disagree with a balance on an SOA, you may use this

form to tell us why you were unable to ask for an informal

review of the NOA you previously received. If we determine

that your failure to respond within 45 days was due to

reasonable cause, we will then evaluate your concerns over the NOA you received. Reasonable cause means that you

exercised ordinary business care but were still unable to meet a department deadline.

We will also accept a separate written request for an informal review of your NOA or SOA. You may mail, email,

or fax your request for informal review to the contact information in your notice or these instructions.

Penalty waiver

We automatically waive your late payment penalty if you

pay your tax and interest within 30 days of the date on your NOA. If you were unable to pay your tax and interest within 30 days of the date on the NOA due to unforeseen

circumstances, you can use this form to request a waiver of penalty if you believe you have reasonable cause. You must pay tax and interest before we can consider waiving any penalties.

Once we receive your request, an auditor will review it to

determine if you qualify for a waiver. We will send you a letter informing you of our decision within 30 days of your

request. If we deny your request for a waiver of penalty, you may request an informal review of our denial by filing

this form within 45 days of the date on our denial letter.

Appeal process and timing

When we make an adjustment to your tax return or amount owed you have the right to request an informal review for the department to review that change.

If you disagree with the adjustment on your NOA, you

must send us a written request for an informal review

within 45 days of the date on the NOA. Your request must

explain why you disagree with our adjustment. Include any documents that support your position.

Once we receive your appeal, it will be forwarded to a

department manager to review the adjustment. The manager will review your request and the work of the auditor who made the adjustment and send you a response within 45 days that outlines whether or not we agree with your request.

If you did not send your request for informal review within

45 days of the date on the NOA, we consider it to be a

deemed admission that you agree with our adjustment. At that point, you can no longer appeal the adjustment we made unless you demonstrate that you had reasonable cause for missing the 45 day deadline. We will review the

reasons you provide and determine if there is reasonable cause to review the adjustment. Once our review is

complete, we will send you a response with our decision.

If we determine that you had reasonable cause to miss your appeal deadline, you can file an informal review of the

adjustment we made to your return.

Our response will inform you if we agree or disagree with your appeal. It will also explain our reasons for disagreement so that you understand our decision. If you disagree with our decision, you may request further review by sending Form APLS102F,

Notice of Referral to the Office of Dispute Resolution, to the Office of Dispute Resolution within 45 days from the notice of determination date. The Office of Dispute Resolution is an

independent division within the department which may hear

taxpayer appeals at the request of the taxpayer. They can either act as a mediator or issue a final department decision.

Form APLS102F is available at MTRevenue.gov.

Filing this form

Email this form and supporting documents to

DORObjections@mt.gov. Mail to:

Montana Department of Revenue

DOR Objections

P.O. Box 7149

Helena, MT

Administrative Rules of Montana: 42.2.510, 42.2.512

Questions? Call us at (406)

The Montana Apls101F form is designed for taxpayers who wish to request an informal review of a Notice of Assessment (NOA) or to seek a waiver of penalty. The NOA is typically the first notification sent by the Department of Revenue when there are adjustments to a tax return, including changes to amounts owed or refunds. By using this form, taxpayers can formally ask for a review of these adjustments or request relief from penalties under certain circumstances.

This form should be filled out by any taxpayer who has received a Notice of Assessment and disagrees with the adjustments made. Additionally, if a taxpayer is unable to pay their tax and interest on time and believes they have reasonable cause for this, they may also use the form to request a waiver of penalties. It is also applicable for joint filers, where both spouses need to provide their information.

Taxpayers must submit the Apls101F form within 30 days of the date on their Notice of Assessment. This timeframe is crucial, as failing to submit within this period is considered an admission of agreement with the adjustments made. If a taxpayer misses this deadline, they must demonstrate reasonable cause for the delay to have their appeal considered.

When completing the Apls101F form, taxpayers should provide:

Once the Apls101F form is submitted, it will be forwarded to a manager for review. The manager will evaluate the appeal and respond within 30 days. This response will outline whether the department agrees or disagrees with the taxpayer's appeal. If the appeal is not submitted within the 30-day window, the taxpayer may lose the right to contest the adjustment unless they can prove reasonable cause for the delay.

If a taxpayer disagrees with the department's response to their appeal, they have the option to request further review. This can be done by submitting Form APLS102F, which is a Notice of Referral to the Office of Dispute Resolution. This request must be made within 30 days of the determination date provided in the department's response. The Office of Dispute Resolution can either mediate the situation or issue a final decision.

Yes, taxpayers are encouraged to attach any documents that support their appeal when submitting the Apls101F form. If there is not enough space on the form to provide all necessary information, additional pages can be included. This supporting documentation can significantly strengthen the case for a waiver or adjustment.

The Apls101F form can be submitted via email or traditional mail. To email, send the completed form and any supporting documents to DORObjections@mt.gov. Alternatively, taxpayers can mail the form to the Montana Department of Revenue at the following address:

Montana Department of Revenue

DOR Objections

P.O. Box 7149

Helena, MT 59604-7149

If you have additional questions or need assistance regarding the Apls101F form, you can contact the Montana Department of Revenue at (406) 444-6900. For individuals who are hearing impaired, Montana Relay can be reached at 711 for support.